Most retirement models are mathematically correct. The assumptions underneath them are not.

Every financial projection for retirement rests on a quietly optimistic premise: that a professional's income will follow a long, stable, upward arc. Salary grows modestly. Savings compound. The corpus arrives on schedule. The math is sound. But the math is only as reliable as what you feed it — and one of its most critical inputs is now under pressure in a way it has never been before.

The input is career stability. And AI is repricing it fast.

The assumption everyone is carrying

For most of the last three decades, a career in India's knowledge economy followed a reasonably predictable arc. Skills accumulated. Seniority compounded. The income curve, on balance, went up and to the right.

That arc was real. The question is whether it describes the next thirty years as accurately as it described the last.

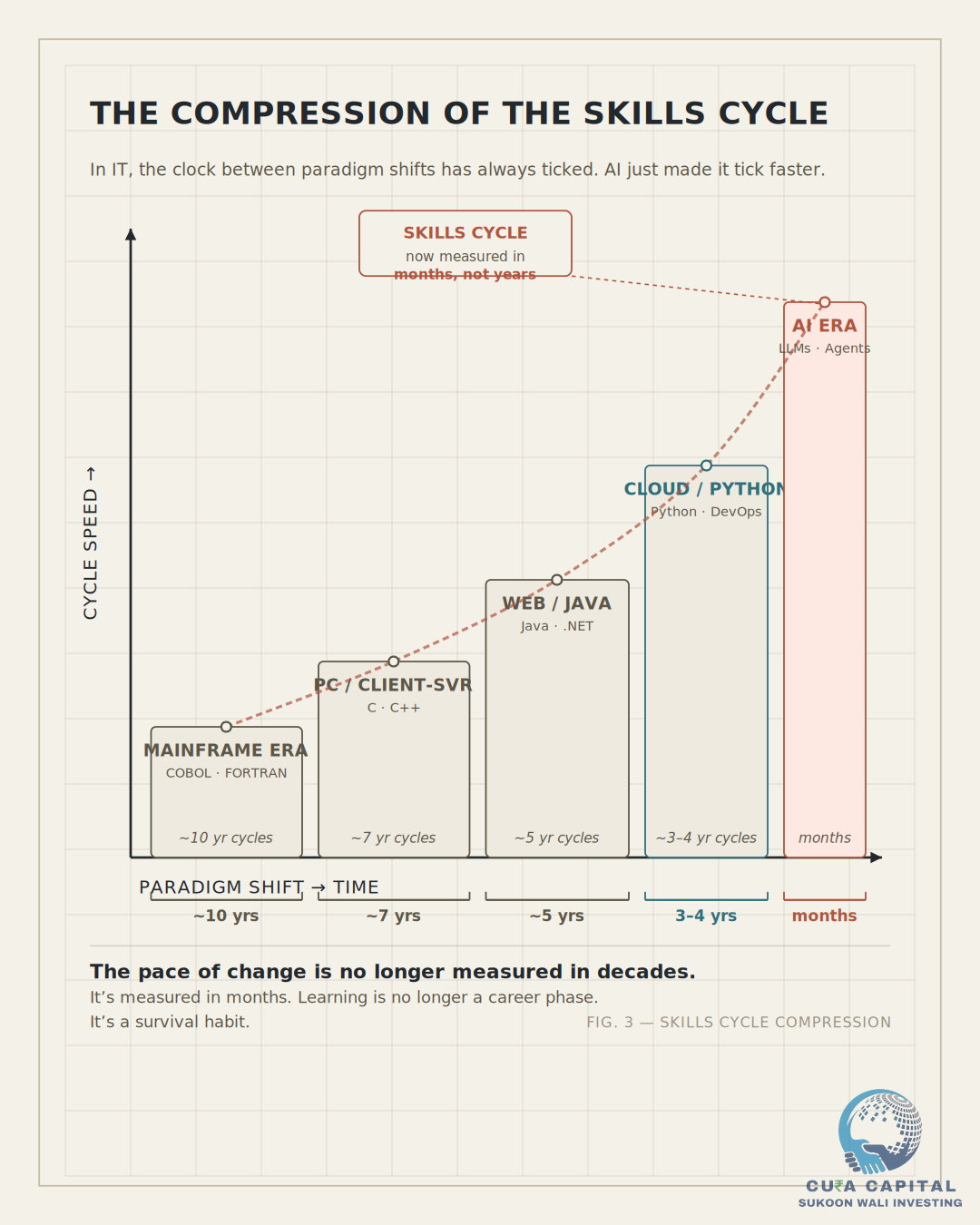

The IT industry has always had a faster skills cycle than most. Every four to five years, the paradigm shifted: mainframe to client-server, C++ to Java, on-premise to cloud. Each transition required reskilling, but professionals had time — typically years to adapt, upskill, and reposition.

What has changed is the pace.

AI has compressed that cycle from years to months. The same computational leverage that makes AI powerful also makes it extraordinarily fast at making yesterday's skills redundant. The skills that earn a professional a senior role today are not becoming irrelevant over a career. They are becoming irrelevant within one.

Puneet Chandok, President of Microsoft India and South Asia, put it plainly at the Microsoft AI Tour last December: today's professionals are likely the last generation to enjoy stable, single-field careers lasting decades. He was not predicting mass unemployment. He was pointing to something more precise — that careers will increasingly follow a portfolio model, with skills being bundled, unbundled, and rebundled faster than any traditional planning model accounts for.

What the data is already showing

This is not a distant threat. The numbers from the past eighteen months tell a structural story.

Over 55,000 tech workers globally lost their jobs in the first quarter of 2026 alone — an average of 736 per day. Nearly 80% of those cuts came from US-headquartered companies, but the India impact has been disproportionate. India's IT sector has seen tens of thousands of roles reduced since 2025, affecting not just freshers but mid-career and senior professionals.

TCS cut 12,000 employees as it pivoted to an AI-first model. Wipro reduced fresher hiring guidance by 20–25%. And the pattern of cuts has shifted: it is no longer random. Routine work, process-intensive roles, and increasingly, the layers of experienced management built to supervise them — these are the positions being structurally removed, not rotated.

The most pointed recent example is Opendoor, a US-based real estate technology company that shut down its entire India operation on June 11, 2026 — 250 employees across Chennai and Bengaluru. The CEO's rationale was precise: they had unified their fragmented systems and built small AI-native teams in the US. The offshore operational workforce — once a competitive advantage — was no longer needed. One team with the right tools replaced a headcount that once required hundreds.

Opendoor is not large. But the template it is demonstrating is not small.

The labour-arbitrage model that powered India's IT services boom was built on a fundamental equation: a large, skilled workforce at lower cost could execute workflows that were expensive to run in the US. AI breaks that equation — not by making the workers less capable, but by making the workflow itself redundant.

The crisis hiding in plain sight

Against that backdrop, the retirement data becomes alarming rather than merely surprising.

India is currently living through a striking paradox.

Retirement has surged to the single most important financial priority for Indian households — yet only 37% of Indians actually hold a retirement plan, down sharply from 67% just two years ago. The median retirement corpus sits at ₹28 lakh. The typical target is ₹1 crore. That is a 3.6x gap — and it widens to 8x for higher-income households who believe their earnings insulate them.

Nearly 77% of respondents in a recent survey said they had not sought professional financial guidance for retirement. Among the highest earners — those making above ₹25 lakh annually — most still preferred managing it themselves.

This is a planning crisis. But underneath it, there is a more structural problem that the surveys do not name directly: most retirement plans being built today are still modelled on career assumptions that were formed in a different economy. One where the income curve was stable. One where a skills disruption happened once in a decade, not once every few months.

Where this intersects with retirement planning

Now bring this back to the retirement plan sitting on most professionals' phones or in their financial planner's spreadsheet.

That plan assumes a salary. It assumes the salary grows. It assumes the professional stays employed in a field roughly proximate to their current one, for something resembling a full career.

What it does not model is: what happens if the income curve bends?

Not collapses. Not disappears. Just — plateaus at 42 instead of 52. Dips during a year of forced reskilling at 38. Restarts at a lower base after a pivot at 45. In the conventional retirement model, these are edge cases. In the emerging career reality, they are becoming features of the landscape.

A plan that stress-tests market volatility but ignores income volatility is, at best, half a plan.

Consider what income disruption actually does to a retirement corpus: a 35-year-old earning ₹30 lakh annually, saving consistently, expects to reach a certain corpus by 60. If their income plateaus three years earlier than projected, or they take an 18-month reskilling sabbatical at 42, or their role is restructured and they restart at a lower base — the corpus doesn't just shrink. The compound effects of those early-career disruptions ripple through every subsequent year of accumulation.

The mathematics of compounding work in both directions.

The four assumptions worth stress-testing

For any knowledge professional building or revisiting a retirement plan in the current environment, four assumptions deserve explicit scrutiny:

1. Career continuity. Does the plan account for the possibility of involuntary reskilling periods, career pivots, or role disruption? A plan assuming uninterrupted income until 58 or 60 carries more risk today than it did five years ago.

2. Income curve shape. Most plans assume income grows at a steady rate. If the skills premium on existing expertise is compressing — and the data suggests it is — the income curve may be flatter, or more volatile, than assumed. That changes both the accumulation horizon and the corpus target.

3. Emergency buffer adequacy. The conventional guidance of three to six months of expenses was calibrated for a world where career disruption was a once-in-a-lifetime event. If reskilling cycles are becoming more frequent, the buffer needs to be deeper, more accessible, and factored into the long-term plan rather than treated as a separate emergency account.

4. Reskilling as a financial decision. The choice to invest in a new skill, take a sabbatical to retrain, or accept a temporary income reduction to reposition for a higher-trajectory path has a measurable financial return. That return is almost never modelled in a retirement plan. It should be — because the alternative, staying in a role whose value is declining, has its own silent financial cost.

The provocation worth sitting with

Most Indian IT professionals will stress-test a system architecture before shipping it. They will review a business case before approving it. They will model multiple scenarios before making a significant technical decision.

The retirement plan gets built once, updated rarely, and stress-tested almost never.

The retirement plans being carried forward today were largely designed for the career assumptions of the previous decade. Those assumptions were reasonable then. They are worth revisiting now — not with panic, and not with pessimism, but with the same rigour that knowledge professionals apply to everything else they build.

Because the bug in the retirement model is not in the math.

It is in what the model assumes the future looks like.

And that assumption just became a great deal more uncertain.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Investments in securities markets are subject to market risks. Please read all related documents carefully and consult a qualified investment advisor before making any investment decisions.