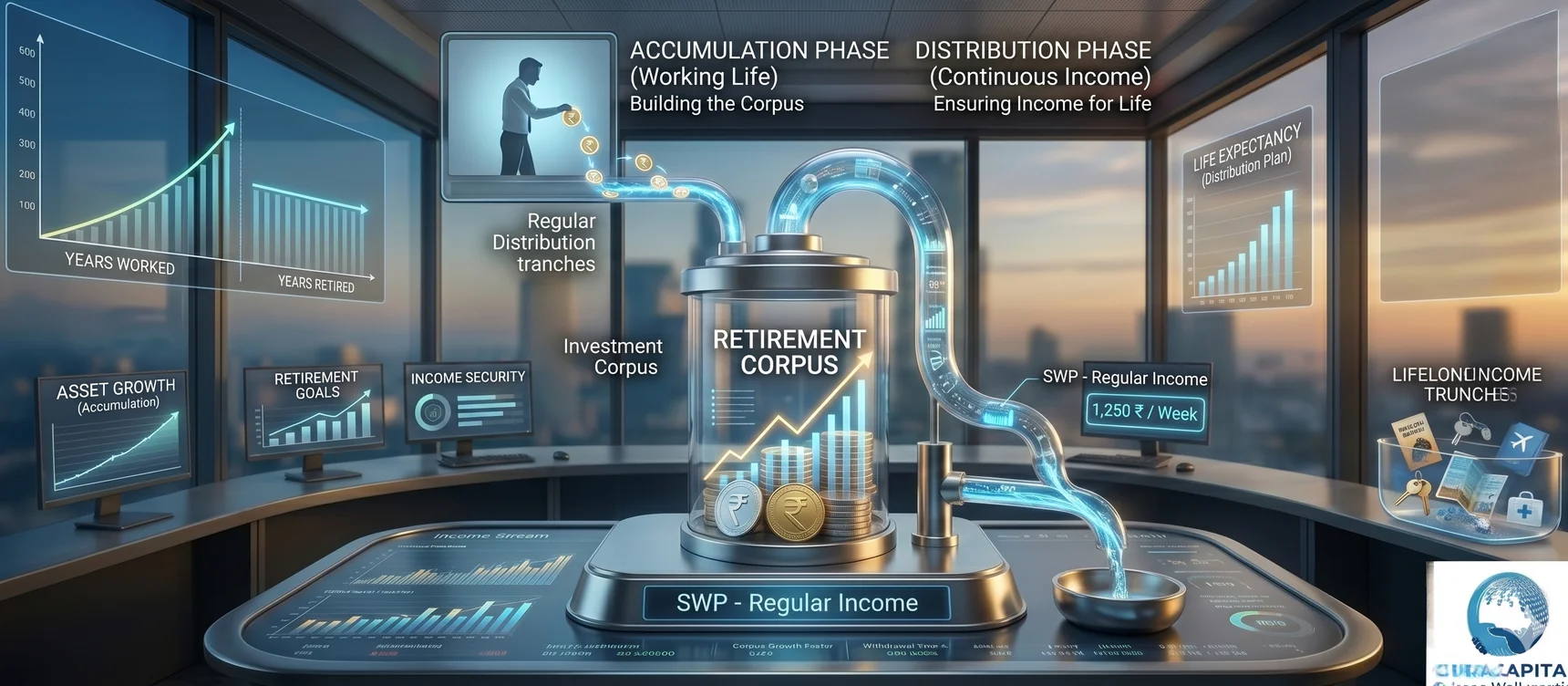

Imagine investing a lump sum once and receiving a steady income every month for the rest of your life — without your corpus running out. That is the promise of a Systematic Withdrawal Plan (SWP). While it sounds too good to be true, a well-designed SWP can genuinely deliver financial freedom in retirement when structured correctly.

Most Indian investors default to Fixed Deposits for retirement income. Safe as FDs feel, they have a hidden enemy: taxation. Every rupee of FD interest is taxed at your income slab rate. For someone in the 30% bracket, a 7% FD effectively yields just 4.9% — barely ahead of inflation. SWP, by contrast, lets your corpus keep growing in equity markets while taxing only the gains, and only at 12.5% for long-term holdings. The difference compounds dramatically over a 20-year retirement.

What Is a Systematic Withdrawal Plan (SWP)?

A Systematic Withdrawal Plan is a facility offered by mutual fund houses that allows investors to redeem a predetermined amount from their investment at regular intervals. You choose the amount, the frequency (monthly, quarterly, or annually), and the fund — the AMC does the rest, crediting withdrawals directly to your bank account.

Think of SWP as the mirror image of a SIP. Where a Systematic Investment Plan drips money into a fund, an SWP drips money out of it. The critical difference from a full redemption is that only a small portion of your units is sold each time — the rest remain invested, compounding at market returns. This is what makes SWP so powerful over long horizons.

There are two types of SWP:

- Fixed SWP: You withdraw a predetermined amount at every interval, regardless of market conditions. Best for investors who need a predictable monthly income.

- Capital Appreciation SWP: You withdraw only the gains above your original investment. Principal stays fully intact. Suitable for investors who want to preserve capital and only spend returns.

How Does an SWP Work?

The mechanics are straightforward. Each withdrawal date, the fund house calculates how many units need to be redeemed at the current NAV (Net Asset Value) to equal your requested withdrawal amount. Those units are sold and the proceeds are credited to your bank account, typically within 1–3 business days.

For example, if your fund's NAV is ₹500 and you want to withdraw ₹25,000 per month, the fund redeems exactly 50 units (₹25,000 ÷ ₹500). If the NAV rises to ₹550 next month, only 45.45 units are redeemed — meaning your corpus depletes more slowly as markets go up.

Worked Example

Invest ₹50 lakh in an equity mutual fund expecting ~10% annual returns. Set a monthly SWP of ₹25,000 (₹3 lakh/year = 6% withdrawal rate). After 20 years, you would have withdrawn a total of ₹60 lakh — and your corpus would still stand at approximately ₹67 lakh, larger than when you started. The remaining corpus grew because the fund's 10% return outpaced your 6% withdrawal rate.

A well-designed SWP can outlive you — the key is withdrawing less than your portfolio earns.

SWP vs Fixed Deposit: Why the Numbers Don't Lie

For decades, retirees have parked their corpus in FDs for the perceived safety of guaranteed returns. But the tax inefficiency of FD interest quietly erodes wealth over a long retirement. SWP from an equity fund, while carrying market risk, offers meaningfully higher post-tax income for the same corpus. Consider a retiree in the 30% tax bracket with ₹50 lakh to invest:

| Factor | SWP (Equity MF) | Fixed Deposit |

|---|---|---|

| Expected Returns | 10–13% p.a. (market-linked) | 6.5–7.5% p.a. (fixed) |

| Tax on Income | LTCG @ 12.5% (above ₹1.25L exemption) | Taxed at slab rate — up to 30% + surcharge |

| Effective Post-Tax Yield* | ~8.5–11% (for 30% bracket investor) | ~4.5–5.25% (for 30% bracket investor) |

| Inflation Protection | Strong — equity grows with economy | Weak — FD rates often lag inflation |

| Principal Safety | Market risk; mitigated by diversification | Guaranteed (up to ₹5L per bank, DICGC) |

| Flexibility | Pause, increase, or stop anytime | Penalty on premature withdrawal |

| Corpus Growth | Remaining units continue to compound | No growth — interest is paid out separately |

*Illustrative. Actual returns vary by fund and market conditions.

Tax Treatment of SWP Withdrawals

Each SWP withdrawal is treated as a partial redemption of mutual fund units — not as "income" the way FD interest is. This distinction is crucial for tax efficiency.

For equity mutual funds (where equity exposure is >65%):

- Units held > 1 year: Long-Term Capital Gains (LTCG) at 12.5%, with the first ₹1.25 lakh of gains in a financial year fully exempt.

- Units held = 1 year: Short-Term Capital Gains (STCG) at 20%.

For debt mutual funds (post-April 2023 amendment): All gains are added to your income and taxed at your applicable slab rate, removing the indexation benefit that previously made them attractive. For retirees seeking tax efficiency, equity or hybrid funds remain the better SWP vehicle.

Importantly, only the gain component of each redemption is taxed — not the full withdrawal amount. If you redeem a unit originally purchased at ₹400 for ₹500, only the ₹100 gain attracts LTCG. This makes effective tax incidence far lower than it appears on paper.

How to Set the Right Withdrawal Rate

The single biggest risk with an SWP is withdrawing too much, too soon. If your withdrawal rate consistently exceeds your portfolio's returns, you'll deplete your corpus earlier than planned — especially dangerous during a prolonged market downturn early in retirement (known as sequence-of-returns risk).

A commonly used benchmark is the 4–6% annual withdrawal rule: withdraw no more than 4–6% of your initial corpus each year. For an equity fund expected to deliver 10–12% annually, this leaves 4–8% for corpus growth even after withdrawals. Over 20–25 years, this can result in the corpus ending larger than it started.

Factors that affect your ideal SWP amount

- Expected portfolio return: Higher-equity portfolios support higher withdrawal rates; debt-heavy portfolios require more conservative rates.

- Inflation rate: At 6–7% annual inflation, a fixed ₹25,000/month withdrawal today will have the purchasing power of ₹12,000 in 15 years — consider stepping up withdrawals periodically.

- Investment horizon: A 30-year retirement requires a more conservative withdrawal rate than a 10-year horizon.

- Other income sources: Rental income, pension, or part-time work reduces dependence on SWP and allows a lower withdrawal rate, giving your corpus more room to grow.

Who Should Use an SWP?

SWP is not for every investor. It works best for those who have built a meaningful corpus in equity or hybrid mutual funds and need a structured, tax-efficient way to draw income from it without liquidating everything at once.

SWP works best if you—

- Have a corpus of ₹25 lakh or more invested in equity or hybrid mutual funds.

- Have an investment horizon of 10 years or more and can stay invested through market cycles.

- Are comfortable with short-term NAV fluctuations and don't need 100% capital guarantee.

- Are in the 20% or 30% income tax bracket and want to reduce tax on retirement income.

Consider alternatives if you—

- Need an absolute guarantee on principal — Senior Citizen Savings Scheme (SCSS), PMVVY, or FDs may suit better for that portion of corpus.

- Have a short investment horizon (under 3 years) or need the entire corpus within a foreseeable deadline.

Step-by-Step: How to Set Up an SWP

- Build or consolidate your corpus. Invest a lump sum (or accumulate via SIP over time) into an equity or balanced advantage fund with a solid long-term track record.

- Choose the right fund. For a 10+ year retirement horizon, diversified equity or hybrid funds are ideal. Conservative hybrid funds suit investors who prefer lower volatility.

- Decide your withdrawal amount and frequency. Calculate 4–6% of your corpus annually. Divide by 12 for monthly withdrawals. Leave a buffer — don't max out the limit.

- Set up the SWP through AMC or your broker. Log in to the AMC's investor portal or your demat/MF platform (Zerodha Coin, Groww, MFCentral, etc.). Navigate to the SWP section, enter your withdrawal amount, start date, and end date (or "until redemption").

- Link your bank account and review annually. Ensure your registered bank account is correct. Review your SWP annually — as your fund grows, you may be able to step up withdrawals to keep pace with inflation.

The Bottom Line

A Systematic Withdrawal Plan is not just a retirement tool — it is a financial freedom engine. When designed correctly, with an appropriate withdrawal rate and the right fund selection, your corpus can keep growing even as you draw from it month after month. Over a 20-year retirement, the difference between a well-structured SWP and a simple FD can run into crores — not because of exotic strategies, but because of compounding, tax efficiency, and staying invested in productive assets.

The earlier you start building the corpus, the more comfortable your SWP can be. If you are within 5–10 years of retirement or have already retired and are looking to structure your withdrawals intelligently, speaking with a our advisor can help you design an SWP tailored to your specific income needs, tax situation, and risk tolerance.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Investments in securities markets are subject to market risks. Please read all related documents carefully and consult a qualified investment advisor before making any investment decisions. Tax rules referenced are based on current legislation and are subject to change.